Mid-Year Update: 2023 Portland Metro Apartment Market

Edited By Clifford Hockley, CPM, CCIM

SVN Bluestone, Principal Broker

As we near the mid-point of 2023, the Portland apartment market has shifted dramatically from 2022 which was a record-breaking year. In the first half of 2023, with ever-increasing interest rates, the sales market has ground to a halt.

Economy in Multnomah County and the Portland MSA

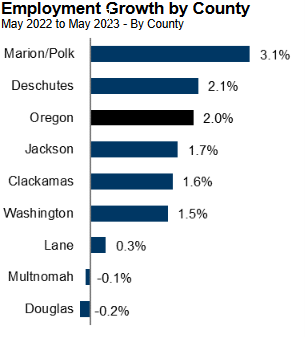

Let’s lay some groundwork. Oregon’s total nonfarm payroll employment grew 2.0%, adding 39,100 jobs over the last 12 months ending in May. Multnomah’s nonfarm payroll employment shrunk by a slight -0.1%, losing an estimated -300 jobs over the same time period. The Portland-Vancouver-Hillsboro MSA’s employment grew 2.6% year-over-year ending in April, which is tied for the 24th fastest percentage growth among the top 50 largest metro areas in the U.S. Metro areas, located in the South region which dominates the top of the list.

The seasonally adjusted unemployment rate in Oregon has started to dip down in the last few months and is averaging 3.7% in May. After having risen to 4.8% at the end of 2022, Oregon’s unemployment rate has declined since January and now matches U.S.’s unemployment rate of 3.7%. Notably, Oregon remains below the 10- and 20-year unemployment rate averages of 5.3% and 6.5%, respectively.

Multnomah County’s and Portland MSA’s unemployment rates both decreased to 3.5% and 3.6% in May, respectively, now below the U.S. trend. Both county and MSA remain below their 10-year averages, both of which are 5.0%. Interesting to note that Marion and Polk County’s employment growth rate year over year, is 3.1%. which is greater than the Portland metro’s 2.6%. (see below chart)

Sales Transactions

Through the first half of 2023, the apartment sales market in Portland Metro has shown an unprecedented slowdown. Through late June 2023, only 35 apartment sales have closed across the four-county Metro Area. When annualized, this sets the pattern for no more than about 70 sales for the year, or down 70% from 2022. To provide some perspective, from 1990 to 2022, there were an average of 208 sales per year with a previous low in 2009 with only 103 total sales.

There are a number of reasons for fewer sales including a dramatic rise in interest rates, greater economic uncertainty, continuing challenges with livability throughout the urban area, some destabilization in the banking sector, and buyers/sellers being unable to agree on current market pricing. Sellers have little urgency to accept lower prices as most owners have a low-interest rate loan, stable rent/vacancy, ample equity, and there are few reasonably priced alternative investments. However, apartments are not alone as all property types have shown a major slowdown in YTD 2023.

The market sale prices have swelled to $280,000 per unit, in comparison to the national index of $250,000 per unit. However, deteriorating lending conditions as a result of the Fed’s ongoing battle with inflation have made deals more difficult to pencil out. This will increase the ask-buy divide and continue to slow down sales.

Nevertheless, Portland remains attractive from a pricing standpoint, relative to some of its other Western gateway peer markets, and some investors have shown a willingness to execute deals creatively in a time of high inflation and high rates.

One example includes Greystar’s 23Q1 purchase of the Heatherbrae Commons in Milwaukie. The institutional giant took on the asset from LivCor through a debt assumption, which allowed them to secure a lower rate executed prior to the Federal Reserve’s current rate hike cycle. The 174-unit community was built in 1995 and fully renovated in 2014. The closing price totaled $49 million ($282,000/unit).

Portland’s transition to a major market for institutional investors chasing both population growth and a diverse economic base has developed over the course of a decade or so. Multifamily cap rates have tightened over the past five years as a result. And this compression did little to deter more capital from entering the market between late 2020 and mid-2022. Some of the largest conventional trades over the past year have been taking place in the suburbs.

In 23Q1, the 100-unit Westridge Lofts in Camas sold for $31 million ($310,000/unit) to a local investor. The community was built in 2021, hovering near full occupancy. In 22Q4, the 347-unit One Jefferson in Lake Oswego sold for $124 million ($357,000/unit). The 4 Star garden complex was built in 1987, with a fully modernized renovation in 2019. Abacus Capital Group LLC acquired the property from Security Properties, Inc. and Pacific Life Insurance Company. Security had originally purchased the asset in 2016 for $78 million and the sale met their return and time horizon goals.

Value-add plays in the region have been popular as well, as investors aim for attractive pricing in a growing market. Buyers appear confident that underserved properties with an added facelift offer attractive upside potential. For example, in late 2022, RedHill Realty Investors purchased the 240-unit Aspenridge Apartments in Vancouver. The closing price was equal to $57.2 million ($238,000/unit). Many of the 1985-vintage units will receive upgrades.

Construction

Since interest rates have increased, the number of units under construction has been declining, with additional declines expected. As of the first quarter of 2023, around 8,500 units were under construction across the Metro Area. In 2023 Apartment completions will out-pace new starts. Fewer lenders are eager to loan on new apartment construction and some developers are having trouble making new units pencil out with changing demographics and balanced fundamentals.

Rents and Vacancies

CoStar reports vacancies are up around 150 basis points year over year and currently sit at 6.2%. Multifamily NW Reports that vacancies are closer to 5.1%. This increase in vacancies is driven by some recent population loss, a high number of recent completions, and increased economic uncertainty. With the increased vacancies, rents have flattened out. CoStar is reporting rents are flat or down slightly year over year. Most of the higher vacancies are concentrated in recent completions and urban areas impacted by livability concerns.

Multnomah County

Faced with red tape, overbuilding, and high taxes, developers are looking closely at sites outside of the Metro area that might allow them to bring product online at a lower price and where there is more demand from buyers and tenants. This is occurring particularly in Vancouver, WA, and Washington and Marion counties.

Rent Control and Other Legislative Changes

The State of Oregon capped annual rent increases at 7% plus inflation for assets 15 years old or older in 2019. This, coupled with other ongoing legislative efforts by the Oregon State Legislature and the City of Portland, may have temporarily helped bring down rent growth from the highs seen in 2015. However, I chalk it up to the intersection of sully and demand.

Summary

In summary, multifamily rental rates in the Portland Metro area are slowing in some areas. Sales are slowing as well, as the interest rate increases coupled with lower rents are making it difficult for buyers to get deals done. This may continue for a good three years until owners of short-term money are forced to refinance and may have to sell if they can’t get the numbers to work.

Quick Stats

Portland Metro

- 12 month delivered units: 6049

- 12 month absorbed units: 2196

- Current Vacancy rate estimated at: 6.5%

Salem, Oregon Metro

- 12 month Delivered Units: 673

- 12 month absorbed units: 249

- Current Vacancy rate estimated at 4.6%

Note:

This article was written with help from Patrick Barry, Costar and Jake Procino, of the Oregon Employment Division. Sources include the below resources.

- Summer 2023 Barry Report – The Barry Apartment Report is a publication covering economic, financial, and valuation trends impacting apartments in the Portland, Oregon metropolitan area. Barry & Associates is a real estate appraisal firm specializing in multifamily appraisals throughout Portland Metro since 1983.

- Costar reports for Portland Metro and Salem Metro

- Multnomah County economic indicators from Jake Procino, Oregon Employment division